Lost in last week’s excitement about arguments over the fish around the UK, the developing second coronavirus wave and the political power battle between Manchester and London was a piece of news which at any other time would be THE NEWS:

Moodys, the credit rating agency downgraded the credit status of the UK, theoretically making it more difficult/expensive for the Chancellor to take out a new credit card on the taxpayers’ behalf, and making access to debt (the growing national debt) more difficult to get a cheap rate.

Moody’s lowered the UK’s sovereign debt rating by one notch to Aa3 from Aa2.

As recently as 2016 the UK was one of the world’s few triple-A rated nations (remember the referendum?) although by the end of 2016 we’d lost that crown and in 2017 suffered another embarrassing downgrade as the government struggled to bring down its debts despite six years of austerity.

It isn’t all bad news though, whilst the ratings agency said it expected that the public finances would worsen as a result of the pandemic, it expects the overall debt burden to stabilise next year, leading it to drop the “negative outlook” attached to the rating to one of “stable”.

Moody’s downgrading of Britain’s credit status was “justified” due to a decline in economic strength in the wake of the coronavirus pandemic and continued BREXIT uncertainty.

The markets also shrugged off the news, perhaps they too are more interested in fish?

Exploring why sovereign credit downgrades might no longer matter as much as they used to, we’re delighted to bring you this guest post under a creative commons license from The Conversation by Professor (Finance) Ghulam Sowar of Keele University:

Why sovereign credit downgrades no longer matter as much as they used to

The decision by credit ratings agency Moody’s to cut the UK’s sovereign credit rating has been a gift to the government’s critics. The agency downgraded the UK from Aa3 to Aa2 on the rationale that its heavy reliance on face-face services would mean that economic growth would be worse than expected because of the coronavirus pandemic.

Moody’s also cited the likelihood of either no Brexit trade deal or a narrow deal, and said the UK is going through the worst “peak to trough contraction” in the G20. It added that the quality of UK legislative and executive institutions, though still high, has “diminished in recent years”.

The downgrade puts the UK on the same credit rating as Belgium, the Czech Republic, Qatar and Hong Kong – three notches below Aaa nations like the US, Germany, Australia and Norway. The other leading agencies, S&P and Fitch, respectively rank the UK as AA and AA-.

Yet the markets responded with a shrug. The pound rose on Monday October 19 after Moody’s made its announcement. Contrast that with the sharp sell-off when Moody’s originally downgraded the UK from Aaa in 2013. This reflects the fact that the new downgrade is unnecessary and happening in a world where ratings agencies’ views on many countries matter much less than before.

The price of money

When ratings agencies cut a country’s rating, it should prompt a sell-off in their sovereign bonds and drive up borrowing costs for the government. In the current interest rate environment, this is far less likely for wealthy countries like the UK.

After the 2007-09 financial crisis, central banks lowered their base rates and engaged in quantitative easing (QE). This is where they “print” money and buy up many government bonds (more recently also corporate bonds). This extra demand causes a shortage in bonds, driving up their prices and lowering the interest rate that issuers pay on them (the yield). The net result is that short-term and long-term interest rates are at historic lows.

In places like the eurozone and Switzerland, the base rate is even negative. This means that when governments issue bonds, they actually pay less than they borrowed. The same can be true for individuals taking out a mortgage – such as at Denmark’s Jyse Bank.

The UK does not yet have negative interest rates, but the Bank of England may introduce them soon. The bank has also been doing more QE in response to the pandemic. This is not a climate in which interest rates are likely to rise.

The UK outlook

If that is the general picture, could anything cause problems specifically for UK bonds? First would be a rise of inflation, but given the pandemic and subdued economic activity this is highly unlikely. Second would be a no-deal Brexit. Setting aside the political choreography, the two main sticking points are state aid and fishing. The two sides have softened their positions on both fronts, so there is a reasonable chance of some kind of deal.

Third would be a significant depreciation in sterling. This is unlikely as it already happened after the Brexit referendum. The fourth risk is international investors dumping British government bonds in favour of those of other western countries. Again unlikely, given that Europe and the US are in the same boat over coronavirus and public debt.

Fifth, investors could switch to Chinese government bonds. But there is a lack of transparency and depth in the Chinese bond market and, more importantly, the Chinese economy is export-oriented. In other words, it depends heavily on strong import demand, which the Europe and US are unlikely to offer consistently for some time.

Finally, there could be an outflow of capital from the UK to emerging markets. But emerging economies are already facing difficulties in servicing their borrowing.

The big picture

Moody’s reasons for downgrading the UK are not unreasonable in isolation. But in a broader context, the arguments about growth challenges apply to most of the developed economies to a lesser or greater extent.

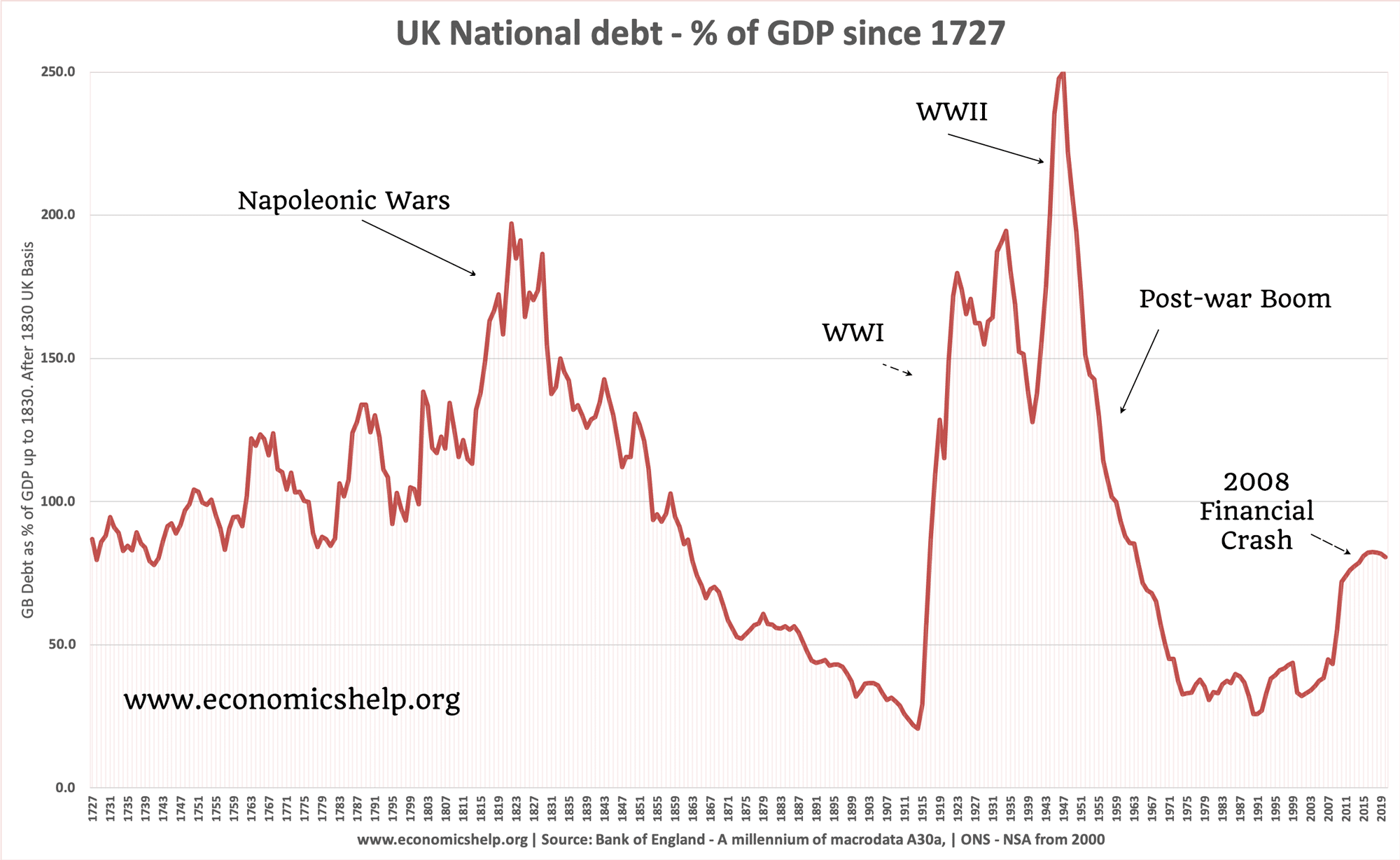

Also, the UK’s debt to GDP ratio is still well below its historical peaks. It was in excess of 200% after the Napoleonic wars and second world war, whereas today it is a touch over 100%.

It is true that consumer and business debt are much higher than in previous generations, but the UK has not defaulted on its bonds since the time of Charles II. Add to this a strong legal system to re-assure investors of legal recourse if the UK did default.

More broadly, inflation could well remain low in a post-pandemic world, resulting in low interest rates for many years. Why not binge borrow, if it doesn’t cost anything in real terms and you can repay over a long period – or even pay back less than borrowed in real terms if inflation increases during the period of repayment?

Some governments are seeing this as a rare opportunity to revitalise their infrastructure. The UK government is ideally positioned to exploit this situation, since the average duration for its bonds to be repaid to investors is long.

At the end of the day, institutions have to keep their money somewhere safe. They would ideally also like a healthy return, but safety may be more important than returns following the global financial crisis and pandemic. If so, government bonds are their best choice and UK bonds are among the best available. Demand for UK government bonds may therefore go up, further decreasing the cost of borrowing.

Moody’s analysis would have made sense prior to the 2008 financial crisis. It does not make sense in today’s world, with historically low interest rates, long average bond durations and public debt still manageable. In short, the downgrade will not have any impact on the UK’s ability to borrow. The agency has not considered the current context or the broader historical picture, and its assessments are not as relevant as they once were.

{kind=link}